Denver Housing Market: Spring Bloom Brings Balance, But Buyers Take Their Time (February 2025 Recap)

The Denver metro housing market is showing signs of a healthy spring awakening. February 2025 brought a welcome surge in inventory, coupled with consistent buyer interest, creating a more balanced landscape for both buyers and sellers. Let's dive into the key trends shaping our market:

Inventory Surge & Steady Demand:

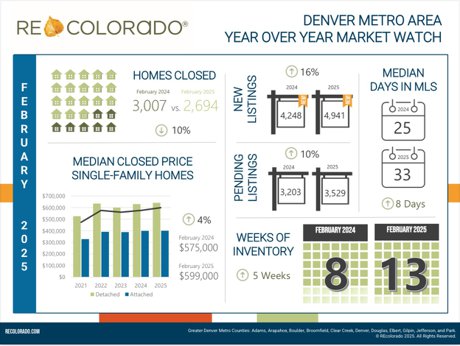

- More Options for Buyers: Sellers added a robust 4,941 new listings, a significant increase year-over-year. This influx of homes provided buyers with a wider array of choices as we head into the traditionally busy spring season.

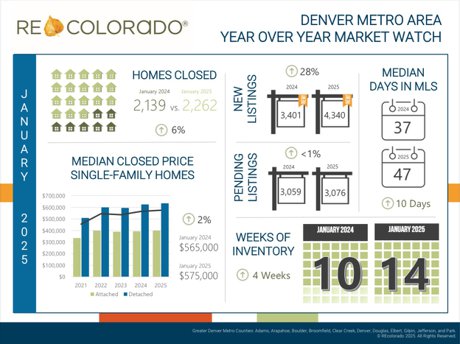

- Consistent Buyer Activity: While buyers are taking their time, they're still active. 2,694 homes closed in February, and 3,529 went under contract, demonstrating continued confidence in the market.

- Price Appreciation Continues: The median closed price reached $599,000, indicating that home values are still on the rise.

- Buyers Taking Their Time: However, buyers are being more deliberate, with homes spending a median of 33 days on the MLS.

Month-Over-Month Momentum:

- Increased Activity Across the Board: Compared to January, February saw a noticeable uptick in activity. New listings jumped by 14%, pending listings soared by 23%, and closed sales increased by 18%.

- Faster Sales Pace: Homes moved off the market quicker, with median days on the MLS dropping by 14 days, suggesting a growing confidence and strategic pricing adjustments.

- Price Growth Continues: The median closed price saw a 4% month-over-month increase.

Denver Metro Rental Market: A Shift in Pace:

- Slower Leasing Activity: The rental market experienced a slowdown, with 216 properties leased through REcolorado's MLS, a 30% year-over-year decline.

- Strong Rental Prices: Despite the dip in leasing activity, rental prices remained strong, with the median leased price increasing 2% year-over-year.

- Tight Rental Inventory: Rental inventory remained tight, with 323 new rental listings entering the market, a slight decrease from both February 2024 and January 2025.

Market Watch Full Report February 2025

What This Means for You:

For Buyers:

- You'll find more options on the market, giving you greater negotiating power.

- However, be prepared to act quickly when you find the right home, as desirable properties are still moving.

- Take your time to do your due diligence and ensure the property meets your needs.

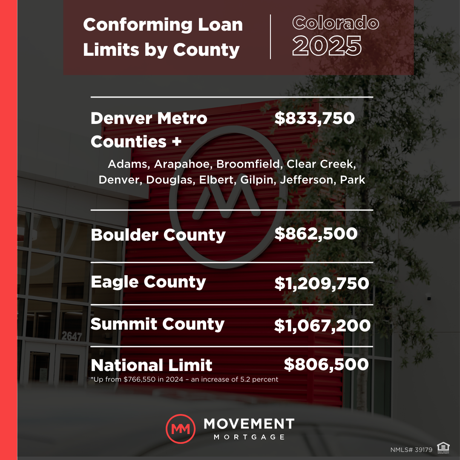

- Monitor mortgage rates, as they will influence your buying power.

For Sellers:

- You can expect continued price appreciation, but be realistic about pricing and prepare for homes to stay on the market a bit longer.

- Present your home in its best light to attract serious buyers.

- Working with a real estate professional to set a competitive price is key.

For Renters:

- Expect a tight rental market and strong rental prices.

- Be prepared to act quickly when you find a suitable rental property.

Looking Ahead:

As we move further into the spring season, it's crucial to stay informed about market trends. Monitoring mortgage rates and buyer activity will be essential for navigating the evolving Denver metro housing market. Whether you're buying, selling, or renting, partnering with Denver Realty Pro, LLC will provide you with the guidance and expertise you need to make informed decisions.

Curious about what’s happening in your neighborhood?

You can create a custom market report to see all active, under contract, and sold homes within your neighborhood!

Considering selling or refinancing your home? Get an INSTANT property valuation now!

We're here to serve all your real estate needs. Contact us today